Getting a loan with a low CIBIL score can feel challenging, but it’s not impossible. Many individuals face temporary dips in their credit scores due to financial hardships, missed payments, or limited credit history. Fortunately, several legitimate ways exist to secure funding even with a low score if you know where to look and how to approach the process strategically.

This comprehensive guide explains how to get a loan with a low CIBIL score, the options available, practical tips to improve approval chances, and key pros and cons to consider before applying.

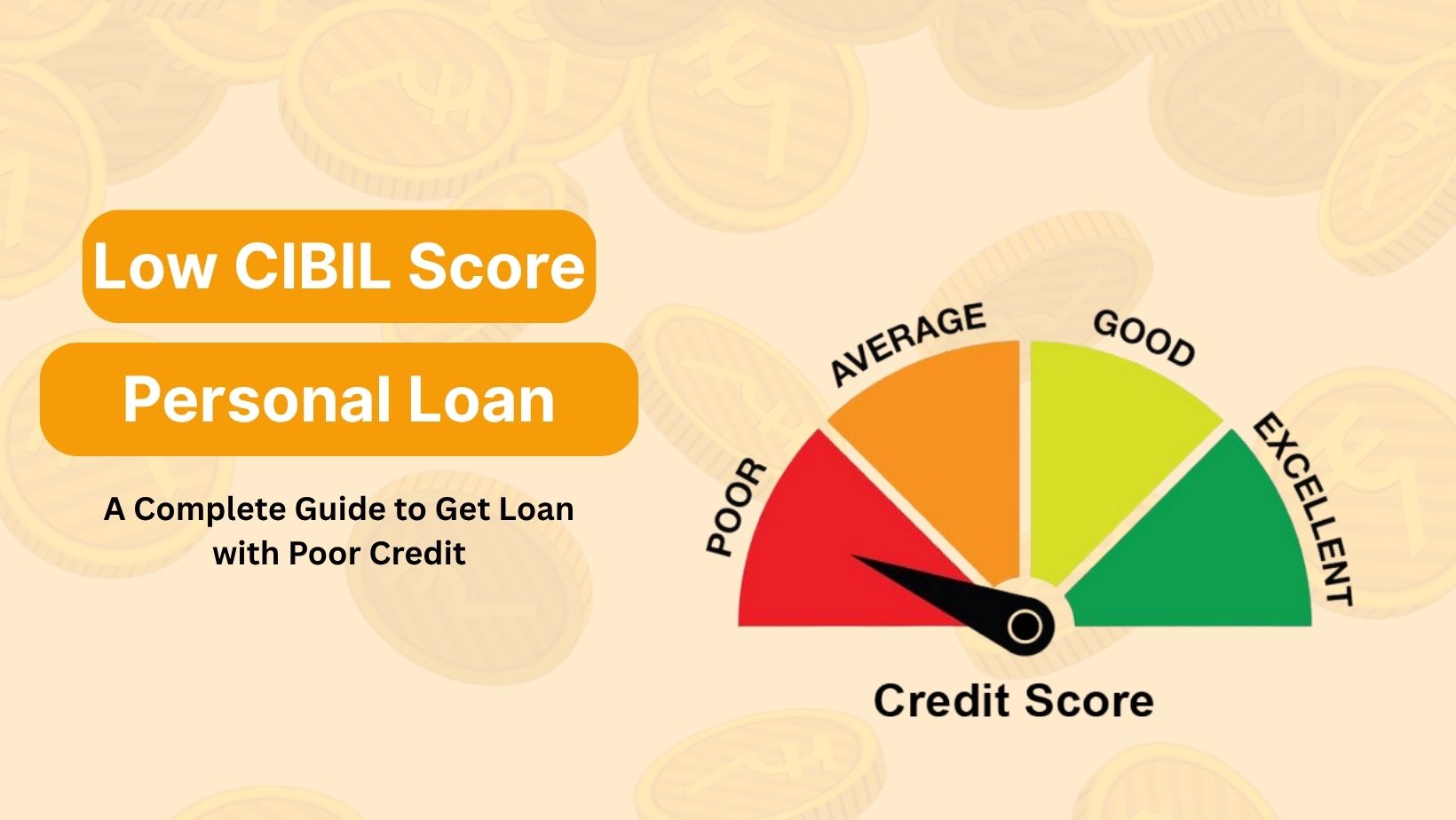

What Is a Low CIBIL Score?

The CIBIL score is a three-digit number ranging from 300 to 900, reflecting your creditworthiness based on your financial history.

- 750 and above – Excellent

- 650–749 – Good

- 550–649 – Fair

- Below 550 – Poor

A low score (usually below 650) indicates higher lending risk. Traditional banks often hesitate to offer unsecured loans to applicants in this range. However, many NBFCs (Non-Banking Financial Companies) and fintech platforms have started catering to individuals with low scores by evaluating alternative data points such as income stability, employment type, and repayment capacity.

Can You Get a Loan with a Low CIBIL Score?

Yes, it’s possible. While a low credit score reduces your options with traditional banks, several alternatives can help you secure personal, secured, or instant loans. These include secured loans against assets like property, gold, or fixed deposits, loans from NBFCs and fintech companies that offer flexible credit policies, co-applicant or guarantor loans to improve your eligibility, and small ticket personal loans or salary-based advances. The key lies in selecting the right loan type and preparing your application thoughtfully.

Top Loan Options for Low CIBIL Score Applicants

1. Secured Loans (Loan Against Collateral)

If your credit score is low, offering collateral increases your chances of approval. Banks and NBFCs are more likely to approve gold loans, loan against property (LAP), or FD-backed loans, as their risk is lower.

Benefits:

- Lower interest rates compared to unsecured loans

- Higher approval chances

- Larger loan amounts possible

2. Gold Loans

Gold loans are among the fastest ways to get a loan with poor credit. Most lenders do not consider credit score as a primary factor since the gold acts as security. You can get up to 75–90% of the gold’s value.

3. Loans from NBFCs and Fintech Platforms

Several NBFCs and new-age fintech lenders focus more on your income and repayment capacity than your credit score. They offer personal loans, instant loans, and salary advances to borrowers with low scores, though often at slightly higher interest rates.

4. Co-Applicant or Guarantor Loans

If you apply with a co-applicant who has a good credit score, the lender’s confidence increases, improving your chances of loan approval. This is especially useful for salaried individuals applying for personal loans.

5. Credit Builder or Small Ticket Loans

Many fintech companies offer small personal loans or credit-builder loans designed to help individuals rebuild their credit scores. Regular and timely repayments can not only meet short-term needs but also improve your CIBIL score over time.

Tips to Improve Your Chances of Loan Approval

Even with a low CIBIL score, the way you apply can make a significant difference. Here are actionable strategies:

1. Check Your Credit Report for Errors

Sometimes, inaccurate or outdated information can bring down your score. Obtain your CIBIL report, and if you find discrepancies, raise disputes to correct them.

2. Apply for the Right Loan Type

Target secured loans or smaller amounts, which are easier to approve with a low score.

3. Show Proof of Stable Income

Lenders may overlook a low credit score if you can demonstrate consistent income and job stability. Attach salary slips, bank statements, or ITR filings to strengthen your application.

4. Avoid Multiple Loan Applications at Once

Submitting multiple applications simultaneously can lower your score further, as each lender performs a hard inquiry. Apply selectively and strategically.

5. Consider a Co-Applicant

Having a co-signer with a healthy credit profile increases the lender’s confidence and can help you secure better interest rates.

Pros and Cons of Getting a Loan with a Low CIBIL Score

| ✅ Pros | ❌ Cons |

|---|---|

| Easier access through NBFCs and fintech lenders | Higher interest rates compared to standard loans |

| Secured loans can help get larger amounts | May require collateral or guarantor |

| Opportunity to rebuild credit with regular repayments | Limited options from traditional banks |

| Instant or quick approvals possible with digital platforms | Stricter repayment terms and penalties |

How to Apply for a Loan with Low CIBIL Score – Step-by-Step

- Check your current CIBIL score and report to understand where you stand.

- Identify the loan type best suited for your profile (secured, NBFC, or co-applicant).

- Collect necessary documents, including income proof, ID, address proof, and collateral papers if applicable.

- Compare lenders online based on interest rates, tenure, and eligibility.

- Apply online or offline through the lender’s official platform.

- Submit documents for verification and respond promptly to queries.

- Receive loan approval and disbursement after assessment.

Quick Ways to Improve Your Credit Score Over Time

- Pay all EMIs and credit card bills on time

- Maintain low credit utilization (preferably below 30%)

- Avoid frequent hard inquiries

- Keep old credit accounts active to show credit history

- Opt for secured credit cards or small loans to build a positive track record

Improving your credit score steadily opens doors to lower interest rates and better loan terms in the future.

Frequently Asked Questions (FAQs)

✔ Can I get a personal loan with a CIBIL score below 600?

Yes, you can, especially through NBFCs, fintech lenders, or by opting for secured loans. However, interest rates may be higher.

✔ Does applying for multiple loans reduce my credit score?

Yes. Each application triggers a hard inquiry, which can lower your score temporarily and signal risk to lenders.

✔ Which type of loan is easiest to get with low credit?

Gold loans and secured loans are the easiest, as they rely more on collateral value than credit history.

✔ Can I get a loan without CIBIL score at all?

Yes, first-time borrowers can apply for secured loans or credit builder loans from fintech platforms to establish credit history.

✔ How long does it take to improve a low CIBIL score?

It depends on your repayment behavior, but noticeable improvements usually occur within 3 to 6 months of consistent on-time payments.

Final Thoughts

A low CIBIL score doesn’t have to stop you from getting the funds you need. By understanding your options, focusing on secured loans, using alternative lenders, and following smart application strategies, you can secure a loan while simultaneously working to improve your credit score. Taking a responsible approach today can open the door to better financial opportunities tomorrow.